When it comes to accounting practices for your business, understanding the difference between GAAP and IFRS is important for managing financials. These two accounting frameworks set the standards for financial reporting, but each serves a distinct purpose depending on your business’s location and growth strategy. For small business owners and expanding enterprises alike, knowing when and how to apply GAAP or IFRS can make the difference between clear financial insights and costly confusion.

Whether you’re expanding internationally and need support with IFRS or staying aligned with GAAP for U.S. operations, the NorthStar Bookkeeping team can help make sure your financials are accurate, compliant, and up to date. Let’s explore how they compare and why this matters for your business.

Why Choose IFRS Over GAAP?

GAAP (Generally Accepted Accounting Principles)

GAAP is the U.S. standard for financial reporting, known for its detailed rules-based approach. It prioritizes precision and consistency, making it ideal for businesses that need rigid compliance structures.

IFRS (International Financial Reporting Standards)

IFRS is the global standard used in over 120 countries. Its principles-based framework allows for more flexibility and interpretation, which can be beneficial for businesses operating internationally or those seeking to adopt modern financial practices.

Related Article: What is GAAP Construction Accounting?

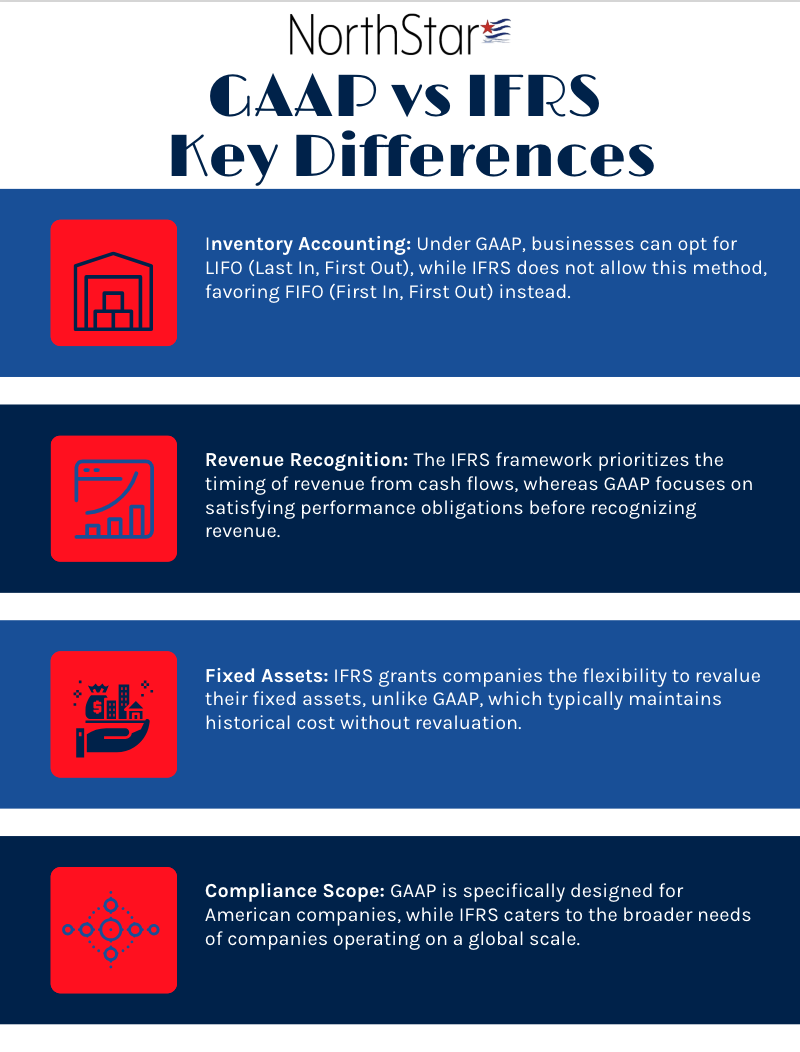

Key Differences Between GAAP and IFRS

- Inventory Accounting: GAAP allows the use of LIFO (Last In, First Out), while IFRS prohibits it.

- Revenue Recognition: IFRS focuses on the timing of cash flow, whereas GAAP emphasizes the fulfillment of performance obligations.

- Fixed Assets: IFRS permits revaluation of fixed assets; GAAP generally does not.

- Compliance Scope: GAAP is strictly for U.S. companies, while IFRS is tailored for global businesses.

Businesses expanding internationally or seeking simplified reporting often prefer IFRS for its adaptability, while GAAP is best for those focusing on U.S. compliance.

“GAAP and IFRS represent two globally recognized financial reporting frameworks, each designed to address distinct regulatory and operational needs. Selecting the appropriate standard requires understanding their differences and aligning them with your business’s strategic goals.”

– Heather Kirstein, Co-Owner, NorthStar Bookkeeping

What Are IFRS/GAAP Consistent Software?

Using accounting software that supports both IFRS and GAAP is essential for efficient bookkeeping. QuickBooks Online, a leading cloud-based platform, offers solutions that can be customized for both frameworks.

Why QuickBooks Online Works

- Versatility: Easily adapt financial reports to align with either IFRS or GAAP standards.

- Real-Time Reporting: Access real-time updates, making it simpler to manage compliance and prepare audits.

- Integration Services: NorthStar Bookkeeping can help transfer your existing financial records seamlessly to QuickBooks Online, ensuring accuracy and efficiency.

With software like QuickBooks, you can maintain clarity and control over your finances, no matter which framework you follow.

Related Article: Which Quickbooks Version is Right for My Business?

Consult NorthStar Bookkeeping for Expert Guidance

Choosing between GAAP and IFRS can feel overwhelming, but you don’t have to navigate this alone. NorthStar Bookkeeping specializes in remote bookkeeping solutions, including helping businesses align with the right accounting standards. From transferring your financials to setting up QuickBooks Online, we simplify the process so you can focus on growing your business.

Schedule a consultation today to ensure your financial reporting supports your goals.